The debut of Apple Pay and similar services was expected to usher in an era of cashless, cardless transactions. So far, it’s not happening.

Sourced through Scoop.it from: www.ibtimes.com

See on Scoop.it – MobilePayments101

The debut of Apple Pay and similar services was expected to usher in an era of cashless, cardless transactions. So far, it’s not happening.

Sourced through Scoop.it from: www.ibtimes.com

See on Scoop.it – MobilePayments101

Google Wallet may not have been the hit Google had hoped, but according to a news report, the Silicon Valley giant may try to breath new life into its mobile payments business by tackling not just the digital billfold, but the digital cash register as well.

[company]Google[/company] has been testing new retail point-of-sale software that works on Android or device or integrates with a store’s existing payment processing system, according to a new report from The Information. The service is called Plaso – pronounced “Play-So” – and it allows customers to pay for goods and services by giving their initials to the sales clerk at the register, The Information’s unnamed sources said.

If that sounds like the failed Square Wallet, you’re right. Plaso appears to be using Bluetooth beacon technology to detect Google’s digital payments apps on smartphones physically in the store or near check out. Like Square…

View original post 453 more words

Mobility is the buzzword for consumer technology at present. From phones to computers, entertainment systems, navigation, and fitness or health tracking devices, being mobile is considered as the norm for practicality.

Source: www.exeideas.com

See on Scoop.it – MobilePointOfSale

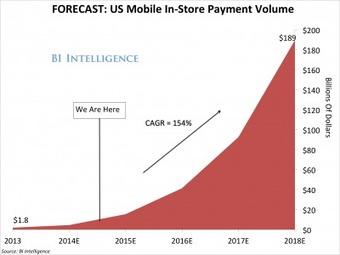

The mobile payments space has fundamentally changed. ;

Source: www.businessinsider.com

See on Scoop.it – MobilePayments101

One of Apple’s most recent products already has an unexpected fan from the competition, who is counting on Apple Pay to help the still-struggling NFC wireless payments business become popular with …

Source: bgr.com

See on Scoop.it – MobilePayments101

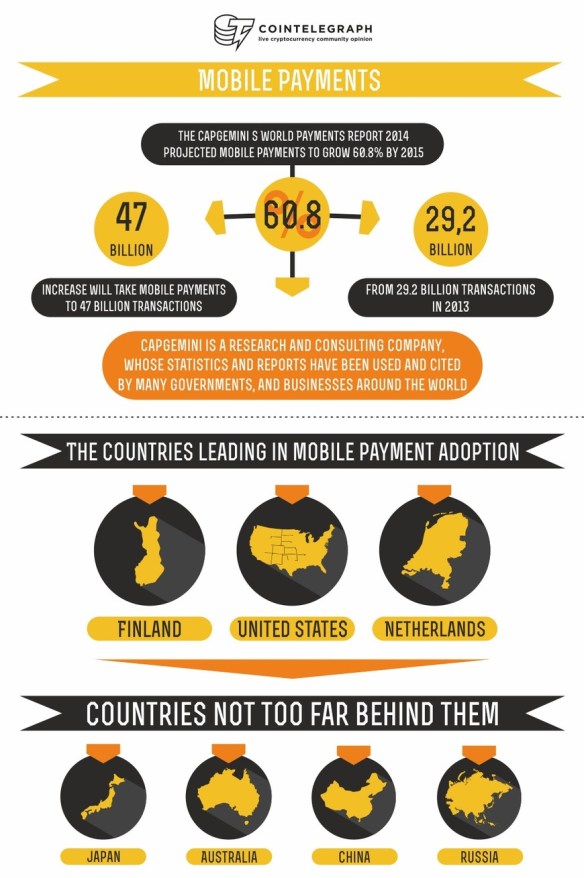

Recently, the Capgemini’s World Payments Report 2014 projected mobile payments to grow 60.8% by 2015.

Source: cointelegraph.com

See on Scoop.it – MobilePayments101

Apples recent and long awaited announcement of Apple Pay which brings mobile payments to the iPhone 6, is an important step forward in Mobile Payments for a number of reasons.

Firstly Apple have been building towards this over a number of versions of iOS and the iPhone, it has not just suddenly appeared with the addition of NFC to the iPhone 6. The iPhone 5S added thumb print recognition, an important biometric security for payments. Before that they added Passbook, which was always meant for more than just boarding passes and event ticketing. Since the first version of the iPhone, iTunes accounts – with Credit Card numbers have been integrated into all Apple purchase transactions. This included the Apple Store app where you can buy accessories in an Apple store straight from your iPhone charging your iTunes account and Credit Card. Now that Apple have over 800 Million Credit Cards in iTunes accounts it made sense to leverage that link to make mobile payments easy for Apple users – simply enter the Card CVV number and you are ready to go with a default payment card.

Firstly Apple have been building towards this over a number of versions of iOS and the iPhone, it has not just suddenly appeared with the addition of NFC to the iPhone 6. The iPhone 5S added thumb print recognition, an important biometric security for payments. Before that they added Passbook, which was always meant for more than just boarding passes and event ticketing. Since the first version of the iPhone, iTunes accounts – with Credit Card numbers have been integrated into all Apple purchase transactions. This included the Apple Store app where you can buy accessories in an Apple store straight from your iPhone charging your iTunes account and Credit Card. Now that Apple have over 800 Million Credit Cards in iTunes accounts it made sense to leverage that link to make mobile payments easy for Apple users – simply enter the Card CVV number and you are ready to go with a default payment card.

Secondly, Apple are leveraging existing payment channels and infrastructure and not trying to disintermediate the banks or card schemes. They have worked with Visa, Master Card and Amex to implement tokenisation to secure the credit card number and transaction data, making this implementation of Apple Pay more secure than physically using your Credit Card. They will utilise the existing EMV Chip and Pin payment infrastructure which already supports contactless (and hence NFC) payments at Point of Sale. Even though the USA still significantly lags the rest of the world in EMV adoption, things are changing quickly and with liability shifts the retailers in USA will be forced to follow the rest of the world and implement the new payment infrastructure. Contactless payments have already had a huge uptake in Australia on the back of EMV and Chip and Pin is accepted all over Europe and Asia.

Finally they have made it really secure and easy to add other payment cards to the Passbook wallet by just taking a picture of the card. No card numbers are stored on the phone and the card’s token is stored on the Secure Element chip on the phone for transactions. Even if the phone is lost or stolen, tokenisation, thumbprint authentication and being able to erase your data with Find my iPhone will overcome any fears of misuse. Surely that is even more secure than plastic cards in a physical wallet?

So it is now clear that NFC (and the Secure Element) was just the final piece in the puzzle of Apples long term mobile payments strategy of giving their users a secure, easy to use and pervasive way of using their iPhones (and Apple Watch) to pay at Point of Sale and Online. Only question now is when is it coming to Australia? It shouldn’t take too long given the infrastructure already in place – just waiting on Visa and Master Card (and the banks)…

Apple didn’t just deliver one mobile wallet at its iPhone 6 and Apple Watch launch event on Tuesday. It delivered two. Its new Apple Pay service, which will launch on the iPhone 6 and iPhone 6 Plus in October, combines two mobile payment methods that are often conflated to represent entirely different types of transactions: using your phone in lieu of plastic to pay at the cash register, and buying goods online over your mobile phone.

[company]Apple[/company] will bridge the two using a unified wallet that consumers will actually want to use and merchants will actually want to accept, Apple CEO Tim Cook said during his keynote (check out Gigaom’s liveblog for all the details from the event). The problem with previous mobile wallets, Cook said, is that they’ve been designed around self-interested business models – for instance, driving dollars into carriers’ own wallets, in the case of Isis/Softcard…

View original post 570 more words